I’m bald. December is “toboggan time” for me. I lose them typically. I depend on them like an appendage. After just a few maddening minutes of looking as I’m strolling out the door, I succumb to eventual embarrassment by discovering one proper there in my coat pocket, ready patiently.

Perspective could be like this. It’s proper there, however we misplaced it. We had it however now it’s vanished, leaving panic. Invariably, we are able to even invent false narratives. “I guess Ashley put it someplace!”

In our short-attention-span-theater world, it’s straightforward to lose perspective on mortgage charges. Like a procuring cart with a nasty wheel, we’ve got a pure tendency to drag our expectations in a route that won’t observe actuality. As a pilot, you’re taught to belief your devices, not your emotions. With monetary issues, we should always belief the information, not the intestine.

In that spirit: What’s the Mortgage Fee Resting State? The place ought to we align our expectations for the traditional state of mortgage rates of interest?

A well-recognized remark from homebuyers is one I’ll dub “The Refinance Chorus.” The chorus finds its voice when a shopper opts for a disadvantageous long-term charge as a result of they’re planning to refinance when charges come again down subsequent yr. I’ve heard a gentle refrain of The Refinance Chorus since mid-2022. Hell, I in all probability hummed just a few bars myself.

For context, a no-points rate of interest is increased than one the place the purchaser pays some semblance of low cost factors. In the event you plan to carry your mortgage for an extended interval (normally 3.5 to 4 years or extra), it’s higher to pay some quantity of low cost factors and earn your a refund over the period of the mortgage. In the event you imagine you’ll maintain the mortgage for a shorter interval, save your cash and take a better/no-points charge on your comparatively shorter period financing instrument.

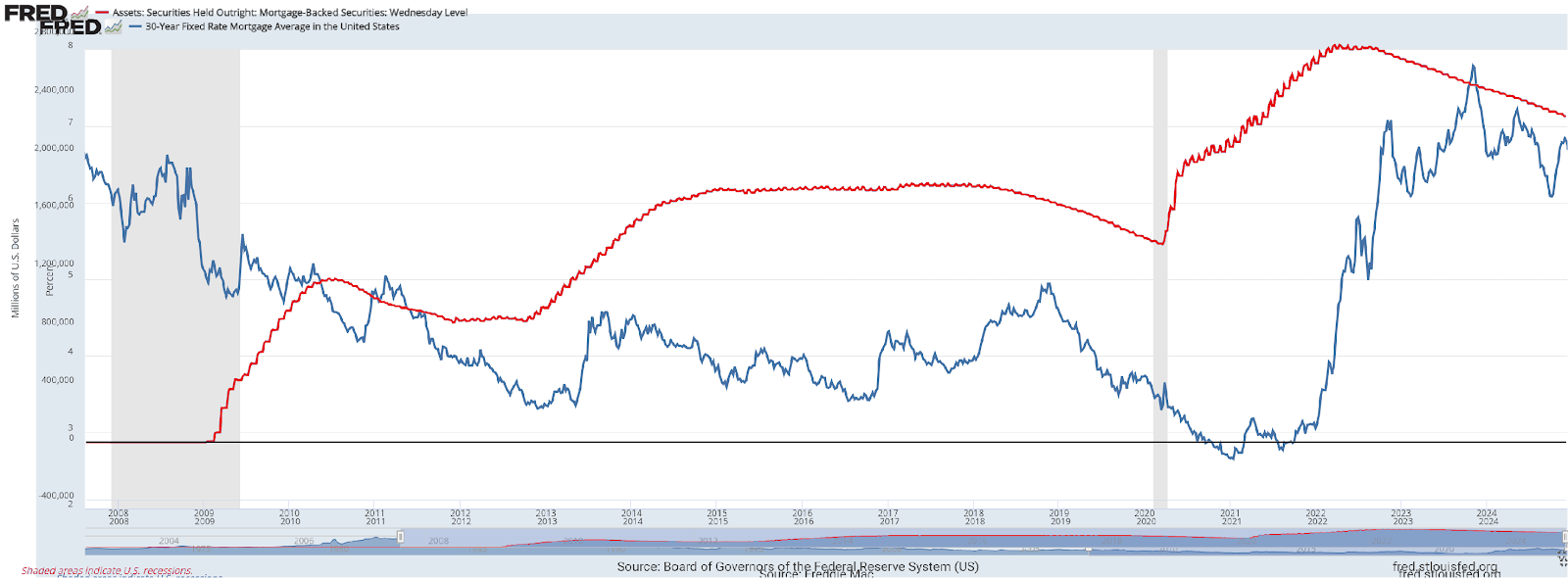

Beneath is a chart of the 30-year fastened mortgage charge since 1971.

And right here’s the identical chart zoomed in from 2008 to current:

You’ll notice that the 30-year fastened dipped beneath 5% for the primary time in fashionable historical past in 2009, about 16 years in the past. Why? What magical financial lever was pulled to drive charges decrease and elevate homeownership affordability to new heights?

My enterprise associate would let you know it’s as a result of the Steelers received the Tremendous Bowl in 2009, the final recreation to characteristic famed commentator John Madden. Students nonetheless debate this coincidence.

Fact be advised, the rationale mortgage charges dipped beneath the Mendoza Line of 5% is because of the actions of our very personal Federal Reserve. In 2008, Bear Stearns and Lehman Brothers sat right down to a banquet of penalties. However the bigger disaster was nonetheless unfolding. U.S. Treasury Secretary Hank Paulson declared “we’re going by way of a monetary disaster extra extreme and unpredictable than any in our lifetime.”

“Too large to fail” was upon us.

By December 2008, Fed Chairman Ben Bernanke, a scholar of The Nice Melancholy and fellow toboggan afficionado, had acted shortly with the Federal Reserve Board to chop the Fed Funds Fee to 0%-0.25%. Nonetheless, Bernanke knew this contagion required a stronger response than slashing short-term borrowing prices. Bernanke wanted the lengthy finish of the yield curve to comply with go well with. How can one management the lengthy finish of the curve?

In January 2009, the Federal Reserve Financial institution of New York modified historical past ceaselessly by stepping off the sidelines and inserting themselves into the sport as beginning Quarterback of the Monetary Disaster. The Fed was now a market participant, shopping for mortgage-backed securities for the very first time. As Madden would say, “don’t fear concerning the horse being blind; simply load the wagon.”

The Fed declared intent to buy $1.25 trillion in mortgage-backed securities (MBS), a transfer that ought to decrease long-term rates of interest, making borrowing cheaper to stimulate exercise. They hoped the actions would additionally carry stability to the monetary system by offering liquidity, the lifeblood of a contemporary economic system.

Spoiler alert.

It labored.

Whew.

Thinker Francis Bacon wrote “typically the remedy is worse than the illness.” Within the case of too large to fail, I’ll take the remedy. The illness would’ve crippled, crushed and cratered the USA economic system. This was a “no-milk-on-the-shelves” second, and I genuinely imagine historical past will decide Bernanke kindly. However Francis’ phrases nonetheless resonate. Medicines depart unintended effects.

The Fed’s actions had been known as “Quantitative Easing.” Depart it to economists to take one thing completely historic and make it sound like a laxative. Quantitative Easing 1 (QE1) led to spring of 2010. Earlier than let’s imagine our 2011 New Yr’s resolutions, QE2 had begun. The Fed’s second spherical of stimulus included purchases of $600 billion in US Treasury securities. This system would proceed till mid-2011.

Like Brett Favre and retirement, typically we don’t know when to give up. In September 2012, the Fed dedicated to QE3, a $40 billion per 30 days buy program for mortgage-backed securities focusing on assist for the housing market. This spherical of quantitative easing would persist longer than the others, till October 2014. From then to the pandemic, the Fed continued to reinvest funds from its holdings into new MBS. Not fairly a continuation of QE3 however no exodus both. Consider it like microdosing for the securities markets. Don’t steal that. It’s mine. I made it up.

The Fed’s dovish public assertion of intentions to maintain rates of interest low coupled properly with their historical past of subbing themselves into the securities contest to steer one other game-winning drive. Buyers feared no evil. Fed to the rescue. Because the 1973 tune by The Spinners goes, “everytime you name me, I’ll be there.”

Beneath is that very same chart reflecting the 30-year fastened since 2008, overlaid with the Fed’s buy of MBS by way of the last decade of the 2010’s (the crimson line). The sub-5% vary occurred for the very first time in 2009. The Mortgage Championship Dynasty of the 2010’s was made potential by the actions of our star Quarterback, the Federal Reserve. Of us, this wasn’t the rule, it was the exception. This model of the Fed for mortgage was akin to Tom Brady for the Patriots. The Patriots haven’t any pure declare to dynasty exterior of Tom Brady. And mortgage charges haven’t any pure proper to historic lows with out their star QB, both.

QE has been changed by QT (quantitative tightening), an economists’ antidiarrheal. The Fed is now not shopping for MBS and although inflation has been tamed, mortgage charges have remained between 6.25-7.25%. Tom Brady retired. The Patriots suck once more. Dynasties finish. Right here begs the query, what’s the Mortgage Fee Resting State?

It’s been so lengthy because the Fed started influencing the housing market, it’s robust to declare a defensible, modern-day reply to this query. However I can let you know for certain, it isn’t beneath 5%.

Again to Sir Francis Bacon and his cautionary story: For the reason that Fed got here off the bench in 2009, they’ve been creating bubbles. They usually nonetheless are. The ultra-low charges of the pandemic have frozen the resale residence market. Hi there, lock-in impact. Present residence gross sales will shut 2024 at 1995 ranges. We’ve stiff-armed a whole technology of Individuals from homeownership.

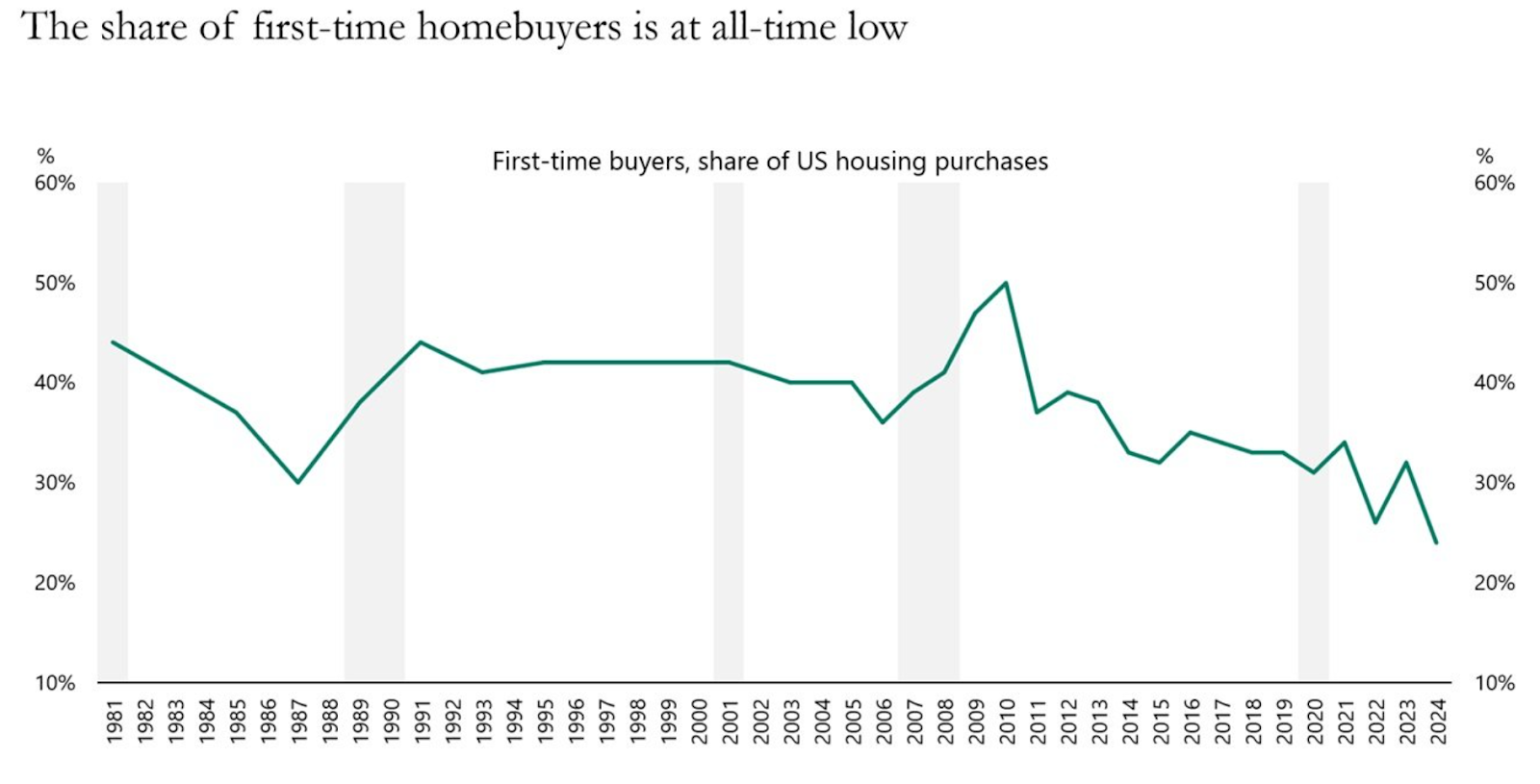

As we speak’s bubble is a requirement bubble. First-time homebuyers now make up solely 24% of all homebuyers, the bottom share because the NAR started monitoring this knowledge (43 years). They’re subbing themselves out of the sport.

The common age of residence sellers was 63 this yr, the best ever recorded. The median age of a first-time home-owner has jumped to 38, up from 35 the identical interval a yr in the past. Within the Eighties, the everyday first-time purchaser was of their late 20s. This bubble can have its personal distinctive and dynamic results for lenders to grapple with for the latter half of the 2020’s.

For now, as mortgage professionals, we are able to do a disservice to our shoppers once we promote narratives with no factual foundation. The answer to fixing any downside begins with a willingness to pull it into the sunshine. Concluding with yet one more Madden-ism: Coaches should look ahead to what they don’t wish to see and hearken to what they don’t wish to hear.

Advisor trumps salesman. Each time.

Mark Milam is the president and founding father of Highland Mortgage.

This column doesn’t essentially mirror the opinion of HousingWire’s editorial division and its house owners.

To contact the editor liable for this piece: [email protected].