[ad_1]

** Word, I am a bit of late in posting my mid-year evaluate as I used to be unplugged a bit for the final couple weeks. Again relationship the publish to its ordinary spot.**

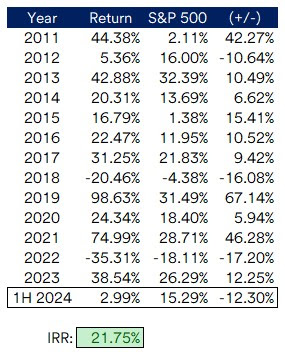

My weblog portfolio is basically flat year-to-date with a acquire of two.99%, properly behind the S&P 500 with a acquire of 15.29%. The damaged biotech basket carried out properly however was typically offset by declines in a whole lot of my legacy holdings and simply malaise in my speculative M&A concepts (crossing my fingers that M&A picks up within the second half). Long run efficiency stays strong at a 21.75% pre-tax IRR.

Closed Positions:

- Fairly a little bit of churn occurred within the damaged biotech basket, I offered Eliem Therapeutics (ELYM), Homology Medicines (FIXX), Graphite Bio (GRPH), Kinnate Biopharma (KNTE), Reneo Prescribed drugs (RPHM), Cyteir Therapeutics (CYT), AVROBIO (AVRO) and Theseus Prescribed drugs (THRX) as every of those had some type of buyout or reverse merger transaction. If there was a CVR part, I held by means of the merger and offered shortly after. A few of these rallied considerably publish reverse merger, however in try to stay to the unique thesis, I typically offered after the shareholder base turned over a bit.

- I obtained spooked out of each Instil Bio (TIL) and Aclaris Therapeutics (ACRS) — though I made a pleasant revenue on ACRS — as each administration groups do not look like following the reverse merger and/or buyout with a CVR technique. Instil Bio has but to promote their new manufacturing facility and I haven’t got confidence within the property valuation, plus TIL included the road of their intention of “Exploring alternatives to in-license/purchase and develop novel therapeutic candidates in ailments with important unmet medical want.” Aclaris introduced alongside their Q1 outcomes “now we have determined to progress ATI-2138 right into a proof-of-concept Section 2a trial in sufferers with average to extreme atopic dermatitis”, nevertheless this one is perhaps price as BML Capital Administration has accrued a major stake and will push ACRS to revisit their go-forward technique.

- Sio Gene Therapies (SIOX) made their liquidating distribution and is now pushed into the non-traded bucket. Equally, Merrimack Prescribed drugs (MACK) made its liquidating distribution, the remaining penny or two is now in a non-traded liquidating belief.

- Pieris Prescribed drugs (PIRS) introduced they’re pursuing an analogous technique as MACK did, minimizing company bills in an effort to increase their money runway lengthy sufficient to seize any milestone funds amongst their disparate portfolio of improvement partnerships. I offered to seize a tax loss, however will proceed to watch this one for a re-entry, if any of their milestones do hit, the return may very well be a a number of of the present market cap.

- MariaDB (MRDB) and Asensus Surgical (ASXC) have been related conditions, money burning corporations with probably useful IP that was topic to a non-binding tender supply, if the tender fell by means of, each may very well be nugatory. Fortunately for me, each offers went to a definitive settlement and I offered every because the unfold tightened to a standard vary.

- First Horizon (FHN) was added shortly after their transaction with TD Financial institution broke in center of the brief lived financial institution disaster final yr, this spring FHN handed over the long-term capital good points mark for me and I booked the revenue. I might see FHN being an acquisition goal for one of many tremendous regional banks making an attempt to make use of an acquisition as a springboard into the next regulatory tier class.

- I ought to in all probability depart the standard merger arbitrage trades to the consultants, I exited Spirit Airways (SAVE) after the judged dominated towards the merger on anti-trust grounds, Albertsons (ACI) hasn’t gone to courtroom but, however below the present administration, probably faces an analogous consequence. In contrast to Spirit, Albertsons is affordable on a standalone foundation and their PE sponsor Cerberus is prone to search liquidity in different methods if their merger with Kroger (KR) fails.

- NexPoint Diversified Actual Property Belief (NXDT) and Transcontinental Realty Traders (TCI) each fall into an analogous bucket for me, actual property corporations buying and selling at very huge reductions to their NAV, however with administration in no hurry to shut these gaps (or just unable to within the present rate of interest regime / actual property market). NXDT has seen some current insider shopping for that improves the story, nevertheless it has been a number of years for the reason that outdated closed finish fund transformed to a REIT and little has been finished to simplify the portfolio or inform the story.

Beforehand Undisclosed Positions:

- I’ve initiated a small place in DMC International (BOOM) which owns three separate and distinct industrial companies. The corporate has introduced a strategic evaluate to promote two of the three companies, forsaking a multi-family residential constructing merchandise enterprise (Arcadia). I did not purchase earlier within the story as a result of it’s unclear to me why Arcadia is chosen one to stay within the public shell, however the scenario modified when Metal Companions (savvy, NOL maximizing conglomerate) lobbed in a $16.50/share supply (shares at the moment commerce sub $14). BOOM has acknowledged the supply and acknowledged they will think about it as a part of their better strategic options course of.

Present Portfolio:

I can be doing a little reshuffling of my private stability sheet, probably withdrawing money from this account within the close to future so maintain that in thoughts once I publish the yr finish outcomes.

Disclosure: Desk above is my taxable account/weblog portfolio, I do not handle outdoors cash and that is solely a portion of my general property. Consequently, using margin debt, choices or focus doesn’t totally characterize my threat tolerance.

[ad_2]