[ad_1]

14 housing tendencies that outlined the yr, together with report home costs, a mortgage fee rollercoaster, and a gross sales sea-saw

The 2024 housing market in some ways mirrored 2023: too few properties available on the market, and never sufficient patrons keen to face excessive costs and mortgage charges. This pushed home costs larger and saved affordability traditionally low – outstanding, provided that 2023 ended because the least inexpensive yr for homebuying on report. Almost 40% of renters thought they’d by no means personal a house.

The market was so troublesome that the median homebuying age jumped to a report 56 years previous – seven years older than 2023. A higher proportion of homebuyers continued to get priced out.

Many homebuyers sat out the yr on the sidelines, ready for affordability to enhance. Others acquired drained of ready and determined to take the leap, even with the market headwinds. The presidential election additionally injected extra volatility and unpredictability.

Nevertheless, there have been some key enhancements, together with extra housing stock, declining inflation, and improved renter affordability.

Under are tendencies, knowledge factors, and visuals that outlined the 2024 housing market.

All knowledge was aggregated from January by November 2024 except in any other case acknowledged. Knowledge got here from Redfin, Lease., the U.S. Census Bureau, FRED, NAR, and/or public information. For questions on metrics, learn our metrics definitions web page.

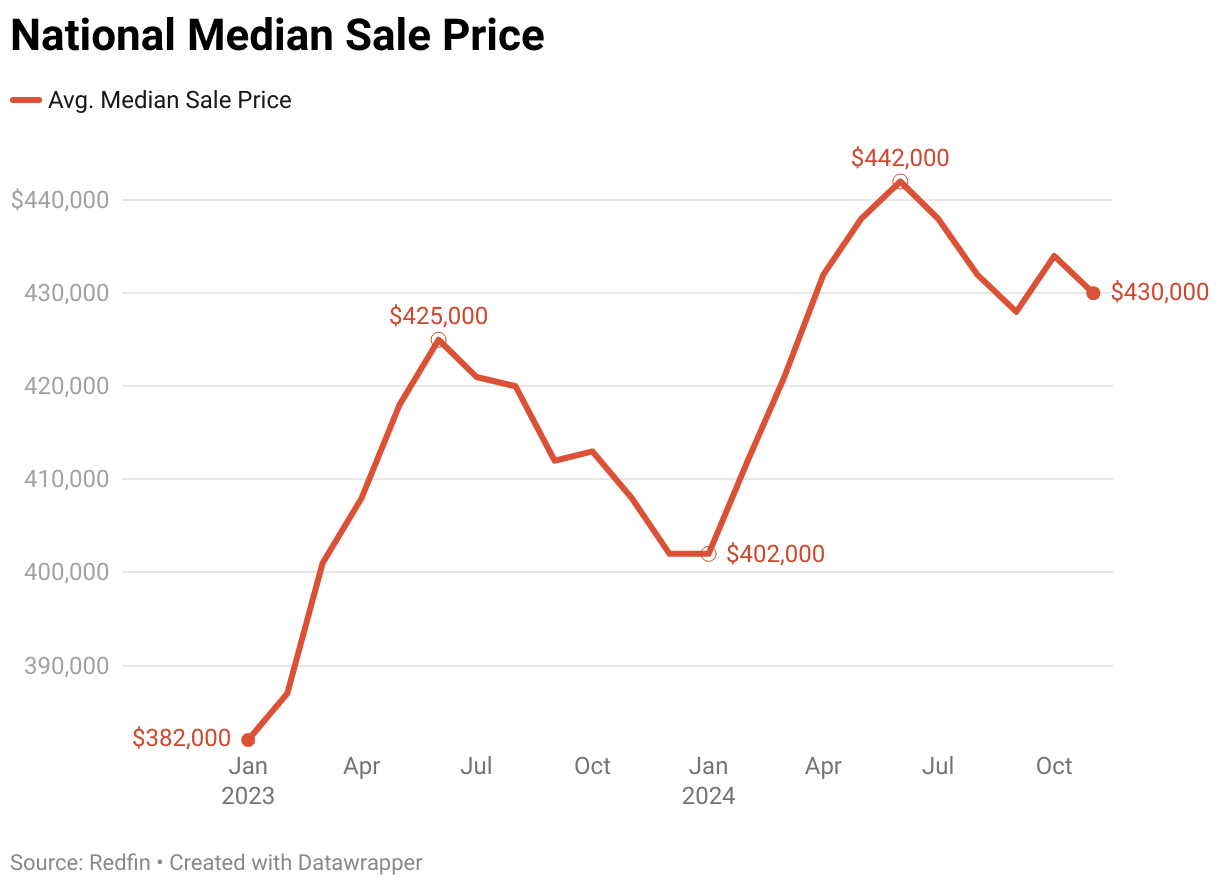

1. Dwelling costs reached consecutive all-time highs

The U.S. median sale worth reached an all-time excessive in July when it hit $442,000, one month after June recorded a excessive of $438,000. Each eclipsed 2022’s report of $432,000. Home costs hit report highs for 9 straight weeks.

When averaging for the whole yr, 2024’s median sale worth of $428,200 far surpassed any earlier yr in historical past, beating final yr’s by $20,000.

“Provide and demand performed starring roles once more this yr,” mentioned Daryl Fairweather, Redfin Chief Economist. “The mix of low provide and lackluster demand gave patrons the truth of a scorching market, despite the fact that few properties modified fingers. This uncommon pattern helped push costs steadily larger all year long, which was unhealthy information for everybody besides homesellers trying to downsize or lease.”

Low-income residents had been hit particularly exhausting. Almost 1 / 4 who made lower than $50,000 needed to skip meals to afford funds.

2. San Jose was the most costly metro space for homebuyers in 2024

Beating out San Francisco, San Jose grew to become the most costly metropolitan space for homebuyers within the nation in 2024. The typical month-to-month median sale worth in San Jose was $1,566,100, up 8.5% ($133,120) from final yr. In any other case, the highest ten costliest markets had been unchanged from 2023.

Home costs usually rose throughout the board, with solely Austin and San Antonio posting year-over-year decreases. Housing affordability grew to become an even bigger disaster this yr, particularly amongst lower-income teams, and was a main difficulty for voters within the presidential election.

- The highest six costliest metros had been all in California.

- Anaheim noticed the most important year-over-year worth enhance within the nation, rising 12.5%.

3. Detroit was the least costly metro space for homebuyers in 2024

The typical month-to-month median sale worth for a house in Detroit was $190,865, up 8.5% ($16,220) from 2023. Costs have risen dramatically for the reason that pandemic, as patrons trying to find affordability fought for a restricted provide. Lots of the most inexpensive metros had been prime decisions for relocating homebuyers early within the yr and have seen giant worth progress for the reason that pandemic.

- All however one of the vital inexpensive metros noticed substantial (>5%) year-over-year beneficial properties.

- 9 of the ten least costly metros had been all situated within the Rust Belt, persevering with final yr’s pattern.

Austin (-2.2%) and San Antonio (-1.8%) posted the one year-over-year drops within the nation. Each additionally noticed the best enhancements in affordability when factoring in wage progress.

4. Dwelling gross sales turned optimistic for the primary time in years

4.62 million U.S. properties offered by November 2024, a slight enhance from final yr however far beneath the 5.62 million offered in 2022. On common, 423,100 properties offered each month this yr, beating final yr’s 417,020.

12 months-over-year dwelling gross sales had been unfavourable each month in 2024 earlier than turning optimistic in September – the primary time in over three years. Gross sales posted stronger will increase of 4.8% in October and seven.2% in November, which was a promising upward pattern main into 2025.

Gross sales probably turned optimistic as a result of mortgage charges dipped considerably in August and September. And pending gross sales, a 1-2 month main indicator of closed dwelling gross sales, confirmed power later within the yr, too.

Dwelling gross sales probably elevated as a result of extra patrons accepted that mortgage charges will hover between 6-7% for now.

- Could noticed the fewest dwelling gross sales, at simply 412,150. There have solely been two months since 2012 with fewer gross sales.

- To shut out the yr, dwelling gross sales posted main will increase in costly West Coast markets, probably as a result of a scarcity of properties intensified competitors.

- Whereas gross sales rose total, they typically fell when mortgage charges spiked. In October, when charges rose from 6.2% to 7%, roughly 53,000 dwelling purchases had been cancelled – the very best share in a yr.

- Two hurricanes and an insurance coverage disaster helped trigger Florida metros to see the largest drops in dwelling gross sales: West Palm Seaside (-9.2%), Fort Lauderdale (-7.9%), Miami (-4.6%), Tampa (-3.9%), and Jacksonville (-3.9%). Alternatively, the drop in gross sales helped enhance provide.

5. Mortgage charges went on a rollercoaster experience

“As soon as once more, mortgage charges dominated the market this yr,” continued Fairweather. “Charges hovered between 6.5% and seven.5%, which scared off many patrons and pushed sellers to carry onto pandemic-era charges.”

Charges had been cussed, too. “Though inflation dropped near the Fed’s 2% goal and we noticed three rate of interest cuts, uncertainty over the election and power of the economic system saved charges elevated,” she added.

Demonstrating how risky charges had been, a weak jobs report in August led traders to push mortgage charges down to six.3%, which prompted a surge in purchaser exercise. Charges fell additional in September, however then shortly rose with the prospect of a stronger-than-expected economic system. We don’t anticipate mortgage charges to alter considerably in 2025.

Consumers who’re cautious of an costly market ought to perceive that traditionally, charges are comparatively common. “When you’re prepared to purchase a house, now could be the time to speak with an agent, get prequalified for a mortgage, and begin your own home search,” suggested April Janas, Senior Mortgage Officer with Bay Fairness, a Redfin firm. “Many markets cater to patrons proper now, with extra choices, much less competitors, and favorable phrases. And if charges do fall in 2025, there are methods to take benefit, together with refinancing your mortgage.”

- The Fed is predicted to chop rates of interest solely twice subsequent yr, lower than beforehand forecast.

- Nevertheless, there may be loads of financial uncertainty attributable to President-Elect Trump’s probably inflationary coverage proposals, together with tariffs, tax cuts, and deportations.

6. Inflation lastly cooled down, however the future is unsure

The Fed’s aggressive fee hikes from 2022 to 2023 lastly helped convey down inflation from report highs. In November this yr, the inflation fee sat at 2.7%, simply above the Fed’s goal however comparatively wholesome traditionally. The Fed responded by issuing three consecutive fee cuts.

Nevertheless, specialists are cautious that inflation may enhance once more subsequent yr, particularly if Trump’s insurance policies pan out. The Fed’s up to date projections for 2025 counsel that they plan to behave with extra warning and lower charges extra slowly.

As rates of interest hovered round 0.5% for the whole thing of the pandemic, inflation took off attributable to provide crunches and elevated client demand. The Fed responded by elevating the benchmark rate of interest 11 occasions over the course of a yr to fight inflation and funky the economic system.

7. Rents held regular

The median U.S. asking lease reached a excessive of $1,649 this yr, just like final yr and a continued reprieve from the pandemic-era rollercoaster. Rents stayed largely flat all yr and dipped main into 2025. The median asking lease throughout all months by November averaged $1,629 – simply $8 greater than final yr.

However when paired with slowly rising wages, leases truly grew to become barely extra inexpensive. Rents for faculty graduates and academics noticed notable enhancements.

The calmer market was pushed by a surge of recent flats accomplished this yr after the development growth in 2021-2022. Now, provide is outpacing demand, and new models are renting extra slowly. Condo building has since slowed.

Rents fell quickest within the Solar Belt and a few coastal metros, which constructed probably the most flats throughout the pandemic. Florida and Texas noticed giant drops this yr. The alternative was true in Rust Belt and East Coast metros, which didn’t construct as a lot and had been then confronted with a provide scarcity.

Importantly, although, rents have remained traditionally unaffordable for the reason that pandemic, skyrocketing by 19% from 2019. A report half of all renters spent greater than a 3rd of their earnings on lease this yr, and 22% spent their complete paycheck. Incomes have lagged behind rents for years, impacting low-income renters the hardest. This lack of affordability, and the chance of dealing with larger rents in a brand new house, has led many renters to remain put.

8. New building slowed down

The U.S. noticed a median of 1.35 million new properties began month-to-month in 2024, down from 1.42 million in 2023 and nicely beneath 2022’s 1.55 million. New single-family dwelling building (excluding leases) fared equally to final yr, peaking at 1.13 million in February.

We anticipate new building to rise subsequent yr, although. “This could have a optimistic impact on provide within the subsequent few years,” famous Chen Zhao, Redfin Senior Economics Supervisor. “New building has lagged for the reason that Nice Recession however has been slowly recovering, peaking simply after the pandemic. Development dipped this yr, however builder confidence has improved heading into 2025.”

Nevertheless, even with post-pandemic enhancements, the nation remains to be experiencing a historic scarcity of inexpensive housing. New building trails nicely behind demand, and the U.S. has a housing scarcity of between 2-6 million models.

Homebuilders have backed off for the reason that pandemic-driven constructing growth, with excessive mortgage and rates of interest hampering purchaser demand and pushing up growth prices. Many builders are actually targeted on promoting the properties they’ve. This helps to elucidate why simply 28% of homes on the market in September had been newly constructed this yr – the bottom share in 3 years.

- California, Oregon, and Utah are amongst states that fall the farthest quick of projected housing wants.

- Housing completions fared barely higher than begins, with an annualized fee of 1,601,000 in November – a 0.2% year-over-year lower.

- Permits to construct single-family properties elevated this yr, however are nonetheless nicely beneath post-pandemic highs.

Knowledge was seasonally adjusted by October 2024.

9. Housing stock posted main beneficial properties

On common, 1.19 million properties had been listed on the market or pending each month by November in 2024, up an enormous 15.8% from final yr. Month-to-month stock peaked at 1.21 million properties in October.

Stock rose for just a few causes: extra sellers determined to check the market; properties sat available on the market for longer; and new housing completions continued to steadily rise.

Energetic listings, a measure of all properties available on the market, have steadily elevated since mid-2023, hitting a excessive of 1.73 million in November. Energetic listings and pending gross sales make up the full housing stock.

Though stock has begun recovering from chronically low provide and the pandemic homebuying craze, it nonetheless sits beneath the historic regular. There aren’t sufficient inexpensive properties available on the market.

Stock is seasonally adjusted and calculated in rolling 90-day intervals, e.g., January 2024 knowledge is the three-month interval from November 1, 2023, by January 31, 2024. Redfin stock information date again to 2012.

10. New listings continued climbing

In step with stock, new listings posted main beneficial properties this yr. A mean of 544,000 properties had been newly listed on the market each month in 2024, up 9% from 2023’s report low. New listings have slowly improved over the previous two years.

The rise in listings took some time to translate to gross sales, although, as excessive housing prices priced many patrons out of the market. It wasn’t till later within the yr that market exercise actually picked up following Fed fee cuts and rises in affordability.

New listings are seasonally adjusted and calculated in rolling 90-day intervals, e.g., January 2024 knowledge is the three-month interval from November 1, 2023, by January 31, 2024. Redfin listings information date again to 2012.

11. Months of provide continued its regular restoration

Whereas stock measures the variety of properties at the moment accessible on the market, months of provide measures the period of time it will take these properties to promote. 4 to 5 months of housing provide is taken into account a balanced market, with extra indicating a purchaser’s market and fewer indicating a vendor’s market.

The typical inventory of housing provide throughout each month in 2023 was 2.8 months, up from 2.5 months in 2023. The market continued to lean in the direction of sellers, however swung nearer to patrons in sure markets, particularly costly metros with restricted demand. Extra inexpensive metros typically noticed the other pattern.

Though provide rose additional in 2024, many patrons needed to combat for each dwelling; by the primary eight months of the yr, simply 2.5% of the nation’s properties modified fingers – the bottom share since a minimum of the Nineties. The pandemic homebuying growth depleted provide, additional hampered by a spike in investor purchases, which has solely began to get better.

“Provide has slowly pulled itself out of its pandemic-infused slide and continued to achieve floor this yr,” added Fairweather. “Nevertheless, it’s nonetheless removed from a balanced market. Consumers and sellers ought to discuss with an agent to find out how finest to navigate their native market.”

- Provide peaked at 3.3 months in January and fared higher than final yr throughout the homebuying season.

Provide is seasonally adjusted calculated in rolling 90-day intervals, e.g., January 2024 knowledge is the three-month interval from November 1, 2023, by January 31, 2024. Redfin provide information date again to 2012.

12. The standard dwelling took greater than a month to promote

Properties spent a median of 39 days available on the market in 2024 – a day longer than 2023. Dwelling gross sales continued their main slowdown from the record-breaking tempo seen in 2021-2022, largely as a result of affordability was so strained.

This slowdown was particularly seen in September, when half of all properties listings had sat available on the market for greater than 60 days. The pattern continued into December. That was up from 43.2% in 2023. Beforehand in Could, greater than three-fifths had been available on the market for 30 days, up from 60% in 2023.

Nevertheless, time-on-market diversified broadly by metro; properties in inexpensive metros typically offered way more shortly than properties in costly metros. For instance, in Could, the standard dwelling in Buffalo offered in simply 8 days, in comparison with 45 days in Austin. Some pricier West Coast markets, like San Jose, noticed jumps in gross sales to shut out the yr, too.

As homebuying affordability worsened, individuals simply wished a house they might afford.

- Many traditionally widespread and inexpensive Solar Belt cities, like Jacksonville, noticed demand skyrocket throughout the pandemic. Now, they’re cooling off and houses are taking longer to promote.

- Could and June had been the busiest months of the yr, with properties spending 32 days available on the market.

- Though they’re slowing down, properties nonetheless promote traditionally shortly on common.

13. Almost 31% of properties had been bought with money in 2024

30.8% of properties had been bought completely with money in 2024 – down from 32% final yr however nonetheless traditionally elevated.

All-cash gross sales usually comply with the identical pattern because the rise and fall of mortgage charges. When charges transfer down, the proportion of all-cash gross sales strikes down; when charges go up, all cash-sales go up. So, as mortgage charges skyrocketed in 2022, all-cash purchases adopted swimsuit. They’ve remained elevated since, however are falling.

Luxurious patrons and traders had been more likely to pay in money.

“By paying all money, prosperous patrons can bypass rates of interest altogether and safe a greater deal,” continued Zhao. “Whereas these are nice advantages, they will contribute to inequality between individuals who personal properties and individuals who don’t, particularly since traders are inclined to gravitate towards lower-priced properties.”

- All-cash gross sales slowly fell all year long from a February peak, as charges dipped and homebuying exercise returned.

- Standard, cheap metros noticed the very best share of money purchases.

- Lots of the costliest metros noticed the bottom share of all-cash purchases, together with San Diego (22.1%), Virginia Seaside (21.9%), and Seattle (20.7%).

14. Investor purchases rebounded following two years of decline

Actual property investor purchases rose for the primary time since 2022 this yr, once they climbed 0.5% in March. Exercise elevated because the yr went on and ended at pre-pandemic ranges – spectacular, given the wild swings the business has seen. Investor purchases surged as a lot as 144% yr over yr in 2021, then dropped as a lot as 47% final yr.

When averaging over the whole yr, investor purchases barely elevated from 2023, hovering simply above 17%.

Traders usually purchase properties to both promote or lease and capitalize on low building prices and excessive demand. When prices are excessive and demand is low, traders normally decelerate purchases.

Since mid-2022, investor market share has posted unfavourable year-over-year progress each quarter, dropping from a report 20% in 2022 to 16% in 2023. Now that home costs are hitting new highs and the shock of excessive mortgage charges is within the rearview mirror, traders are reentering a extra interesting market.

- Traders made more cash in comparison with a yr in the past. In March, the standard dwelling offered by an investor went for 55% greater than they purchased it for.

- Traders backed out of Solar Belt metros the quickest, with Fort Lauderdale (-13.1%) and Miami (-10.6%) seeing among the many largest drops in purchases.

- Though investor market share has declined for the reason that pandemic, it’s nonetheless traditionally very excessive.

- Multi-family properties continued to be the most well-liked amongst traders, with condos coming in second.

Wanting ahead

The 2024 housing market was powerful for a lot of householders and renters, however what does Redfin predict for 2025? Learn our 2025 Housing Market Predictions to be taught extra.

[ad_2]